Top

Search

People also search for:

Stay Inspired with Instagram

Imagine you are a juggler, and you are juggling multiple balls at the same time. That’s what neobanking feels like today. You are managing payments, savings, investments, and budgeting, all in one seamless flow. And you know what’s the best part? You’re not at a risk of dropping the ball either because millions of people are already living this experience with neobanks. Everything is neatly gathered in a single basket, effortlessly designed to give you control, convenience, and confidence.

So, it’s important to know what neobanking is. Neobanks are actually hassle-free banks and a favorite among Gen Z, who prefer everything fast and feature-rich. With everything accessible online, customers no longer need to roam around branches to get what they want. The time-saving and highly convenient framework of neobanks makes them a true game-changer in the modern banking system.

In simple words, neobanks are digital-first banks that deliver core banking through mobile and web, often without physical branches. Some neobanks hold full banking licenses; others partner with licensed banks. Either way, they’re built on modern stacks, which means they offer:

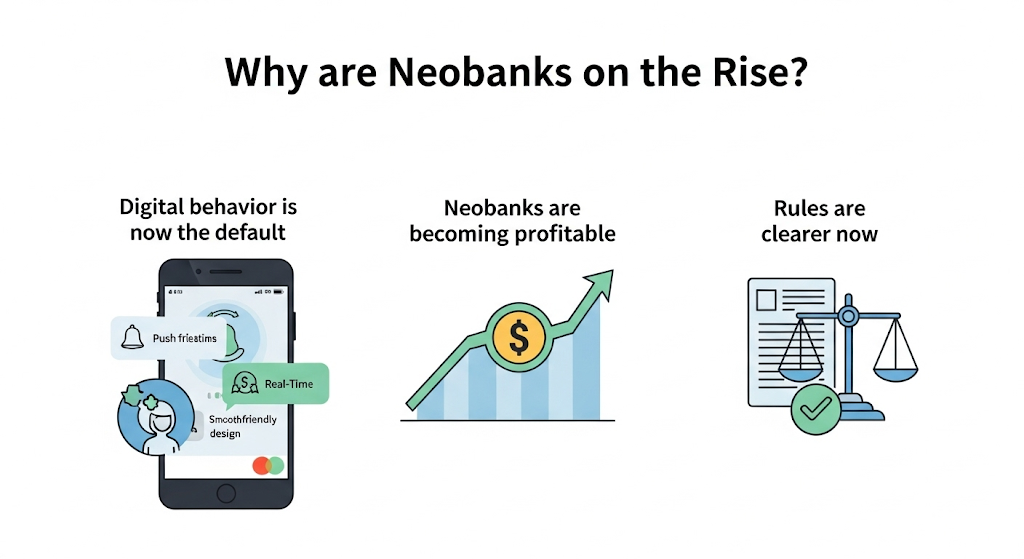

Neobanking is on the rise and will continue to do so. According to Fortune Business Insights, the global neobanking market is projected to grow from $210.16B in 2025 to $3.41T by 2032 (CAGR ~48.9%), with Europe leading the share today. This means that neobanks are not going anywhere in the long run. They are going to change the whole banking experience with their advanced technological setup and inherently evolved framework.

Another leading bank in Latin America, Nubank, reported 118.6M customers in Q1 2025, adding 4 million new customers in that quarter. These users are actively using the Nubank app, giving tough competition to other consumer apps like Instagram and Facebook.

This also suggests that people are becoming more interested in money management and prefer spending time on investing and checking their financial apps instead of just randomly surfing consumer apps.

Besides neobanks, you might also have heard the term challenger banks. Think of them as sisters with different personalities. They are quite similar to neobanks, but there’s a small difference in how they operate. Challenger banks hold a license for digital banking, while neobanks may or may not have a license and often partner with traditional banks to offer a digital-first experience. For instance, Revolut (UK) in its early years functioned as a neobank, while Monzo and Starling Bank (UK) are challenger banks. This blog is going to cover some important themes, such as why neobanking is important and how digital banking will affect the future.

The term neobanking app development refers to new apps and systems that are digital-only banking apps. It means that the customers will manage their money while sitting in their homes. Neobanking app will manage all the activities associated with bank accounts, like opening an account, transferring money, paying bills, applying for a card, checking their balance, and so on, all through a smartphone interface.

Typically, development of a neobanking app will include:

Think of a Digital Banking Solution like a toolbox that powers neobanks. It includes KYC/AML checks, card issuing, account-to-account transfers, risk scoring, personal finance tools, fraud detection, credit decisioning, and APIs. Together, these digital banking solutions make it possible to open accounts in minutes, send instant notifications, automate compliance, and roll out new features quickly.

Real examples show how powerful this model is. Revolut has more than 52 million customers worldwide. In 2024, it reported about $4.0 billion in revenue and $1.0 billion in profit—impressive for a bank that started mobile-first. In the UK, Monzo passed £1 billion in annual revenue in 2025 and recorded strong profits, proving that digital banks can now scale with solid economics.

This is not a small experiment anymore. Neobanking has become a major trend in finance. It is reshaping the banking experience because of its evolved and enhanced tech stack and its tendency to execute processes faster than legacy banks.

Neobanks have changed the whole banking dynamic. They are meeting the customers’ needs with their efficient framework.

The competitive arc: From features to Economics

The first wave of challenger banks won hearts with standout features like:

The second wave is building financially healthy models:

There is no denying that traditional banks still earn most of the profits, but digital banks are catching up quickly by offering innovative, futuristic features.

The emergence of neobanks has changed customers’ relationships with money. Neobanks offer compliant, fully digital experiences (real-time onboarding, modern interfaces, tailored products), and they are redefining established norms and changing the way customers view traditional banking. With more consumers adopting app-based banking, the financial space is changing for the better.

Neobanking isn’t simply an attractive front-end UI. It is a full-stack re-invention of how money moves, how risk is managed, and how products are delivered. Some prominent challenger banks like Revolut, Monzo, and Nubank have proven that digital-first banking can be both popular and profitable. Revolut’s $1.0B net profit in 2021 and Monzo surpassing £1B in revenue are not exceptions. These numbers show that the industry is becoming stable and sustainable.

Moreover, with the right amount of expertise, you can create a scalable and future-focused financial platform. Also, fintech development solutions will allow you to improve operational efficiency and capitalize on new growth opportunities in a rapidly changing financial landscape.

We manage and optimize your IT infrastructure end-to-end.Ensuring stability, security, and operational continuity.

Consult IT Experts

Hi! I’m Aminah Rafaqat, a technical writer, content designer, and editor with an academic background in English Language and Literature. Thanks for taking a moment to get to know me. My work focuses on making complex information clear and accessible for B2B audiences. I’ve written extensively across several industries, including AI, SaaS, e-commerce, digital marketing, fintech, and health & fitness , with AI as the area I explore most deeply. With a foundation in linguistic precision and analytical reading, I bring a blend of technical understanding and strong language skills to every project. Over the years, I’ve collaborated with organizations across different regions, including teams here in the UAE, to create documentation that’s structured, accurate, and genuinely useful. I specialize in technical writing, content design, editing, and producing clear communication across digital and print platforms. At the core of my approach is a simple belief: when information is easy to understand, everything else becomes easier.